Inflation Reduction Act deep dive: New investment tax credit opportunities and elective pay options for health systems

Our summary and deep dive into how heath care organizations can utilize IRA incentives to advance climate- and equity-related work

By Antonia Herzog, Ph.D., Health Care Without Harm Director of Climate Policy and Advocacy

The Inflation Reduction Act (IRA) is the U.S. government’s largest investment in climate action to date, comprising over $369 billion in federal programs and tax incentives to decarbonize the U.S. economy. The IRA allocates funds to improve building efficiency, electrify vehicle fleets, deliver clean energy to the electrical grid, spur domestic clean energy manufacturing, and facilitate the acceleration of infrastructure supporting clean energy deployment.

Barriers to reducing the health care sector’s greenhouse gas emissions have included a lack of knowledge about reliable technological alternatives to conventional fossil fuel-based energy sources, laws that impede clean energy adoption, and a lack of available resources to invest in solutions that combat climate change within the health care sector.

The IRA has the potential to significantly reduce the financial barriers for health systems to procure low-carbon energy alternatives by providing substantial incentives, especially in the form of tax credits that encourage health care organizations to decarbonize.

The health care sector — and nonprofit health care systems specifically, which represent a majority of U.S. health systems — can benefit from the combination of the elective pay provisions coupled with the investment tax credit (ITC) provisions and bonus credits given for compliance with domestic content and prevailing wage and apprenticeship requirements, and investing in low-income and energy communities.

This legislation addresses greenhouse gases attributable not only to buildings, but also to vehicles, manufacturing facilities, and industrial agriculture. The maximum incentives for projects that fulfill every criteria are significant. A relatively small, new project that meets labor and domestic requirements, and is built in a low-income energy community, for example, could qualify for an ITC as high as 70% of the project cost. Larger projects, which don’t qualify for the low-income community bonus, could still be eligible for a full 50% maximum credit.

The health care sector accounts for almost $4 trillion, or 18%, of the U.S. economy and is responsible for 8.5% of all U.S. GHG emissions, with hospitals generating over one-third of those emissions. Health care systems nationwide can play a critical role in implementing the IRA and advancing the domestic clean energy economy. Already, health systems across the country are pursuing health equity goals through livable wage, education, housing, and job creation initiatives in their surrounding communities. By integrating clean energy incentives with incentives for domestic economic growth, job creation, and assistance for low-income communities, the IRA presents a unique opportunity for health care to advance its mission to do no harm and lead the way to a sustainable, low-carbon, and resilient economy.

Below, we outline the details of the IRA’s Elective Pay and Investment Tax Credit provisions, key components of the legislation, that can be used directly by health systems to invest in climate solutions.

Elective pay

Elective pay, often referred to as “direct pay,” changes the game for nonprofit health care systems as they plan to invest in clean energy generation across their real estate portfolios. Previously, clean energy tax credits could only be accessed by developers with tax liability or through partnerships formed with tax equity investors. This approach complicated the process, raised the cost of financing for clean energy projects, limited adoption among smaller-scale developments, and remained susceptible to market volatility.

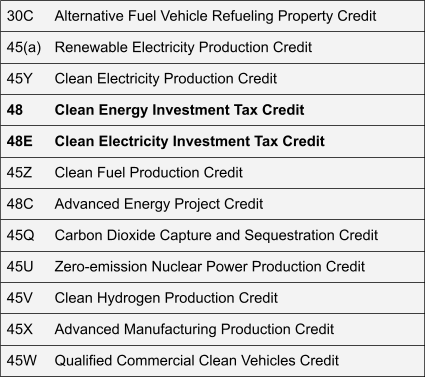

Through the elective pay mechanism, the IRA altered the financial landscape for clean energy investments by opening the door to organizations such as states, political subdivisions, the Tennessee Valley Authority, Indian Tribal governments, Alaska Native Corporations, rural electricity co-ops, and nonprofits with vested interest in the development of net-zero carbon electricity production and energy storage technologies. Nonprofit health care organizations can now use elective pay for the credits listed in Table 1.

Table 1: IRA tax credits with elective pay option

In June 2023, the U.S. Department of the Treasury and the IRS released proposed regulations describing which nonprofit entities qualify for elective pay and the application process by which to obtain the funds. With elective pay, an eligible entity (such as a nonprofit health care system) that qualifies for one of the above IRA tax credits (Table 1) files a notification with the IRS of their intent to claim the credit and then files an annual tax return to claim elective pay for the tax credit. The IRS then pays the nonprofit entity the value of the credit. In this way, elective pay allows nonprofits to apply for and receive federal dollars that were previously not available to them. Health systems can maximize elective pay credits by stacking them on top of other IRA grants and loans to achieve the maximum emissions reduction.

Increasing the deployment of clean energy helps health care systems reduce their energy use and save money. By participating in this climate-smart and fiscally responsible transformation, health systems have the opportunity to step forward as local leaders, modeling climate action and helping improve resilience in the communities they serve.

Domestic content requirements to use elective pay

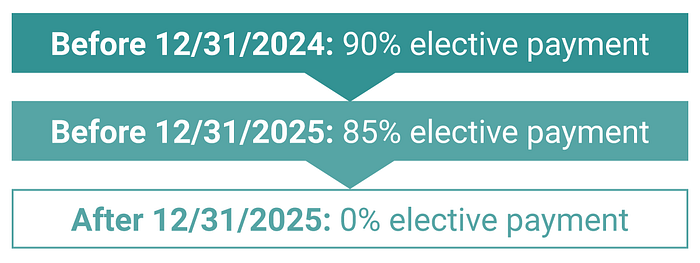

Starting in 2024, nonprofit health care systems that wish to receive the full amount of the elective pay eligible tax credits listed in Table 1 must meet the domestic content requirements for their projects, which are described in the bonus credits section below. Entities that plan to use elective pay and fail to meet the domestic content requirements will receive reduced payments according to the construction timeline outlined in Figure 1.

Figure 1: Reduction in elective pay schedule

Investment tax credits

Credit amount: Base investment tax credit is 6% for the first 10 years, from Jan. 1, 2022, through 2032.

Phase out: The credit value reduces over a three-year period beginning in the first calendar year after the “applicable year,” which is the latter of (i) 2032 or (ii) the calendar year in which the annual greenhouse gas emissions from electricity generation are 75% lower than 2022. Facilities will be able to claim a credit at 100% value in the first year, then 75%, then 50%, and then 0%.

Before the IRA, the renewable energy sector depended largely on power purchase agreements that often involved third-party ownership of the renewable energy asset, which was previously restricted to solar energy projects. The IRA maintains the investment tax credit (ITC) benefits that already existed for solar and expands the types of clean energy technologies that are eligible for the ITC. It also extends the time frame during which the ITC maximum credit is available by at least a decade, from 2022 to 2032. Furthermore, projects smaller than 5 MW can now include the costs for connecting the project to the grid.

As noted above, if the power sector hasn’t hit the decarbonization target of less than 25% of 2022 emissions by 2032, the credits won’t phase out until the target is met, connecting the credits to important, real-world targets.

Clean Energy Investment Tax Credit

Period of availability: Facilities placed in service after Dec. 31, 2021, and beginning construction before Jan. 1, 2025

Credit amount: 6% base credit for all technology types except geothermal heat property

The Clean Energy ITC (section 48) provides nonprofit health care organizations with many more opportunities to offset capital investments in technology-specific projects built before Jan. 1, 2025. Eligible clean energy technologies include solar, geothermal, fiber-optic solar, fuel cell, microturbine, small wind, offshore wind, waste energy recovery, combined heat and power.

Health systems and other nonprofit organizations should note that ITC 48 was also expanded to provide a 6% base tax credit for standalone energy storage (at least 5 kWh), biogas, microgrid controllers (20 MW or less), dynamic glass (electrochromic), and linear generators constructed before Jan. 1, 2025. For geothermal heat pump energy property in commercial buildings, the base investment tax credit of 6% is extended to cover projects constructed before Jan. 1, 2033, scaling down to 5.2% in 2033 and 4.4% in 2034.

Several bonus credit opportunities were included, such as a 10% bonus credit for projects that meet domestic manufacturing requirements for steel, iron, and other manufactured products and componentry, and a 10% bonus credit opportunity for projects in energy communities. The bonus credit structure is described in the bonus credits section below.

Clean Electricity Investment Tax Credit

Period of availability: Available after Jan. 1, 2025, through 2032

Credit amount: 6% base credit for all net-zero or net-negative carbon emission technologies

For organizations that make substantial investments in clean energy technologies after Jan.1, 2025, the Clean Electricity ITC (section 48E, technology-neutral) transitions from the technology-specific approach of the ITC 48 to an emissions-based incentive while maintaining the same bonus credit structures. Project managers should select net-zero greenhouse gas technologies to ensure their clean energy production investments after 2024 can claim this version of the ITC.

Health care organizations can offset operational energy use at the facility level by leveraging the tax incentives included in ITC 48 and 48E through savvy clean energy investments, with a view toward the long-term performance of their owned assets.

Bonus credits

The IRA is a federal investment vehicle that provides tiered incentives for clean energy projects designed to aid in the expansion of the domestic clean energy economy, create new jobs and career growth opportunities, revitalize regions with economic roots in the fossil fuel economy, and prioritize construction in low-income communities. Investment in these areas is rewarded in the form of incremental tax credit bonuses that can be stacked to maximize the financial benefit to the project.

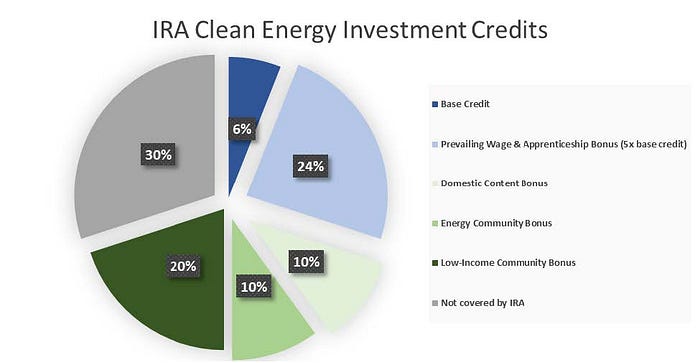

Project owners who wish to qualify for the highest tax credit available will need to incorporate prevailing wage and apprenticeship standards across all future work in order to achieve the 30% tax credit as the base credit amount. However, projects with a maximum output of less than 1 MW, or that were under construction for tax purposes by Jan. 28, 2023, are exempted from these labor standards and have a base credit starting at 30%. The remaining bonus opportunities range from 10%-20% and are dependent on the material content and location of the project as shown and described in Figure 2 below.

Figure 2

Apprenticeship and prevailing wage

The ITC 48 and 48E stimulate the clean energy sector through direct investment in clean energy projects and incentivizing prevailing wage and apprenticeship requirements. This strategy will allow project owners to offset the cost of their projects while creating a need for skilled engineers and young professionals that can grow with market demand. The IRS provided taxpayer guidance, noting that project owners should plan on paying all mechanics and laborers on the job a prevailing wage for the entirety of their project, and for five years after the project is placed into service. Compliance and achievement of this tax credit bonus opportunity require detailed documentation and review of wage rates, employee classification information, and hours worked on the job, but can yield a bonus of up to five times if achieved. For projects that meet prevailing wage and apprenticeship requirements, the 6% base credit amount increases by 24%-30%, as depicted in Figure 2.

Note that projects with a maximum output of less than 1 MW, or that were under construction for tax purposes by Jan. 28, 2023, are exempted from these requirements and automatically receive a base credit of 30%.

Domestic content

The purpose of the domestic content requirement is to encourage the use of American-sourced materials and industries so as to help minimize reliance on imported goods and services, increase American energy security, and withstand the ebbs and flows of the global energy economy. In this way, the IRA encourages project teams to select products that meet thresholds for domestic content, compelling project owners to ensure that their steel, iron, and manufactured products are domestically sourced.

The domestic content requirement applies to any steel, iron, or manufactured product that is a component of an applicable project. To meet this requirement, projects must use products made from 100% domestic steel and iron, and meet the adjusted percentage rule, which stipulates cost thresholds for products manufactured in the United States.

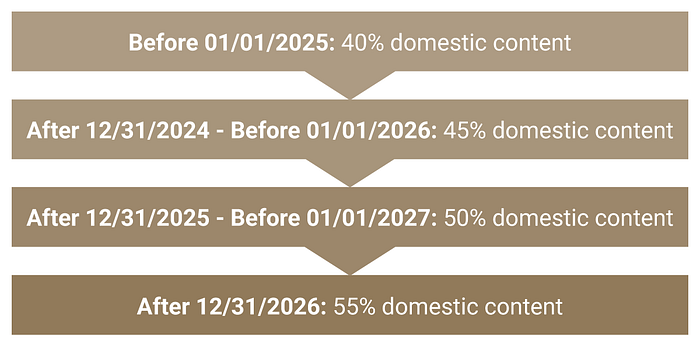

The 100% iron and steel products requirement applies to items directly incorporated into the project that are, “made primarily of steel or iron and are structural in function,” such as steel photovoltaic module racking. For products and componentry to meet the adjusted percentage rule, a percentage of the value of manufactured products and components used in the project must be produced in the United States. Figure 3 displays the requirements for the increasing percentage that applies to the total cost of all manufactured products and componentry produced in the United States, depending on the construction start date. Initially, the total cost of all manufactured products produced in the United States starts at 40%, increasing to 55% over time. Note that for offshore wind projects, the percentage starts at 20% and follows a slightly different schedule over time. This requirement applies to all manufactured items directly incorporated into the project, excluding those that fall under the iron and steel requirement. The calculation of the domestic percentage takes into account a manufactured product’s components but not its subcomponents.

Figure 3: Percent domestic content required to qualify for bonus credit

Meeting the domestic content requirements will qualify a project for a bonus credit from two to 10 percentage points when the prevailing wage and apprenticeship requirements are also met. The U.S. Department of the Treasury and the IRS issued domestic content bonus credit guidance to help determine which energy projects and facilities qualify for this credit.

Health care organizations seeking to access this bonus credit should develop a set of design standards to establish project uniformity and alignment with bonus credit requirements. Project owners should work directly with their project design teams and tailor procurement strategies to prioritize domestically manufactured product adoption and align their new standards with the adjusted percentage timeline.

As a reminder, nonprofit entities that wish to use elective pay must meet the domestic content requirements to avoid a reduction in the tax credit amount (see Figure 1).

Energy communities

To shift toward clean energy sources, the U.S. economy will need to invest in and revitalize regions that have historically produced fossil fuels. The IRS partnered with the Interagency Working Group on Coal and Power Plant Communities and Economic Revitalization to catalog census tracts that meet the energy community criteria:

- Located on a brownfield (These sites require remediation before new development can occur.)

- Coal communities with plants retired from 2010 to 2021/Coal mines closed from 2000 to 2022

- Areas that have 0.17% or greater direct employment or at least 25% of local tax revenues that are related to extraction, processing, transport, or storage of coal, oil, or natural gas, with unemployment at or above the national average in the previous year

Projects placed in service after Dec. 31, 2022, and located within an energy community, will be entitled to an additional two percentage points, up to 10 percentage points, when the prevailing wage and apprenticeship requirements are also met or the project output is less than 1 MW.

Low-income communities

The IRA was developed to modernize and decarbonize the U.S. energy economy, and to lift local economies that need economic assistance with decarbonizing. The IRA seeks to lower energy costs for economically distressed families and communities that have been hardest hit by the rise in the cost of living and inflation of energy costs. These are also the communities most impacted by the effects of climate change. The IRS recently released final guidance regarding the proposed rules concerning low-income communities to help applicants finance projects located in these underserved areas.

The IRA created a Low-income Communities Bonus energy Investment Credit Program to provide 10 to 20 percentage points of additional tax credits on top of the IRC for solar and wind projects below 5 MW that are either meeting environmental justice criteria at the community scale or meeting income criteria at the customer household scale. There are two applicable credits:

- Owners of projects located in low-income communities and Indian land can receive an additional 10 percentage points in tax credits.

- Owners of projects that serve customers who are residents of affordable housing or customers of projects partly dedicated to serving low-income customers can receive an additional 20 percentage points if the facility dedicates at least 50% of the benefits of the electricity produced on-site to low-income households.

Unlike the ITC and the other bonus credits, the low-income communities bonus credit program operates more like a grant program in which prospective recipients need to apply to receive the funds. Treasury may allocate this bonus credit for up to 1.8 GWdc of wind, solar, and connected storage capacity per calendar year. The application for the program will open in the fall of 2023, and awards will start to be made by the end of 2023. Depending on the availability of capacity for more projects, applications for the 2023 program are expected to be accepted through early 2024.

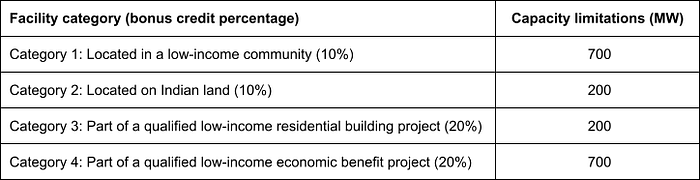

The U.S. Department of the Treasury has split these projects into four categories, as outlined in Table 2.

Table 2: Project categories for low-income bonus credit

Under both ITC 48 and 48E, the low-income communities bonus credits are structured to spur small-scale nonprofit solar and wind projects in low-income areas by restricting eligibility to facilities with 5 MW net output or less. Nonprofit health care systems that have properties located in low-income areas or have interests in investing in microgrids and energy storage systems should tailor the capacity of their facilities and projects to ensure compliance with these bonus credit structures.

This blog was written with input from Mazzetti.